- Offers

- Service providers

- Knowledge base

- Tools

- Arena

- Contact

- Partners

EN

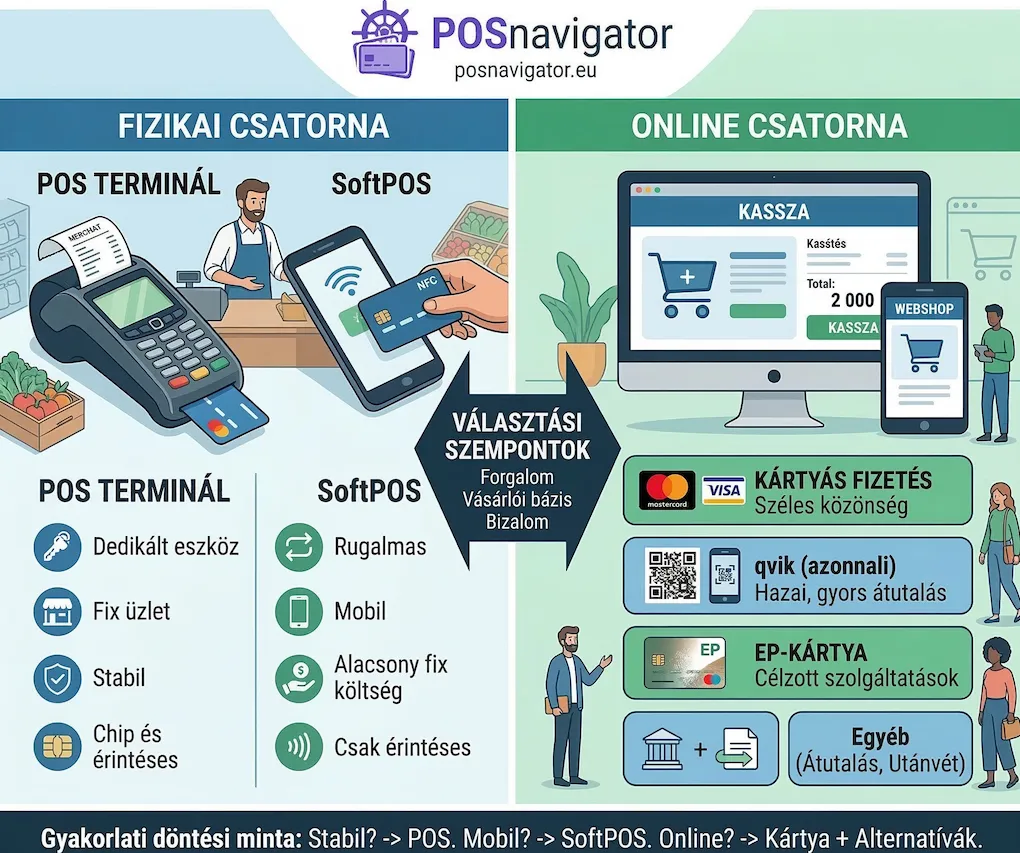

You will choose differently if customers pay in person than if they pay online. The best approach is to separate the physical and online channels and evaluate each based on your own customer situations.

If you already know the channel you need: start a targeted comparison for small-shop POS terminals, SoftPOS solutions, or online payments for webshops.

Below we break down the key selection criteria by channel and show when each option makes sense.

Transaction volume and basket size: if you process steady daily volume, a dedicated POS terminal can be more cost‑effective long‑term. For low or occasional volume, SoftPOS is a faster, cheaper entry point.

Fixed vs. mobile operation: in a fixed store, terminals are stable and predictable. If you are mobile (markets, delivery, events), SoftPOS is more flexible.

Accepted payment methods at the counter: POS terminals typically support contactless and chip payments. SoftPOS generally supports contactless (NFC) only.

Receipts and peripherals: if you need printed receipts, cash register integration, or multi‑lane setups, a POS terminal (or integrated POS system) is more practical.

Cost structure and contract terms: terminals often come with a rental fee and longer contracts. SoftPOS is usually more flexible with lower fixed costs.

Reliability: dedicated hardware is usually more stable and less dependent on phone battery and device condition.

POS terminal: fixed location, daily volume, multiple tills, chip payments, and printed receipt requirements.

SoftPOS: mobile operation, occasional or low volume, fast start, minimal device cost.

Online, the choice of payment methods directly affects conversion. The goal is to let customers pay in a familiar, convenient way — too many options, however, can add friction to checkout.

Customer base: domestic vs. international, B2C vs. B2B? The broader the audience, the more justified multiple options are.

Basket size and trust: higher basket sizes benefit from well‑known, “safe” payment methods.

Checkout friction: fewer steps usually means higher completion rates.

Operations and accounting: payout timing, refunds, and reporting accessibility matter.

The most widely accepted online method with international reach. For most webshops it is a baseline expectation.

Recommended if: you target a broad audience, want fast, familiar payments, or have international customers.

qvik is a collective term for solutions built on the Hungarian Instant Payment System, including QR, NFC, payment links, and payment request flows. The customer approves payment in their mobile bank app.

Recommended if: you mainly serve domestic customers and want a fast transfer‑based option alongside cards.

A specialized card type that can be used only at specific services and contracted acceptance locations.

Recommended if: your target audience uses EP cards (e.g., health or welfare‑related services) and acceptance can materially increase revenue.

These can be useful in specific categories or B2B sales, but are typically slower and more admin‑heavy.

Recommended if: customers explicitly request them or the product category makes them standard.

Physical channel: stable, fixed volume → POS terminal; mobile operation → SoftPOS.

Online channel: make card payments the baseline, then add alternatives that match your customer base (qvik, EP card, bank transfer).

Combination: the channels are not mutually exclusive — you can run a POS in store and an online gateway for your webshop.

On POSnavigator.eu you can compare payment providers in the Hungarian market transparently — by fees, terms, and merchant‑relevant criteria. If you are not sure which solution type fits you, use our cost calculator.

Weekly summary of the best POS terminal offers

We handle your data confidentially. Details in the privacy policy.