- Offers

- Service providers

- Knowledge base

- Tools

- Arena

- Contact

- Partners

EN

The essence of Click to Pay is a frictionless shopping experience: a global digital wallet that is not tied to a specific device (like Apple Pay to the iPhone), but to the user’s profile (email address).

Click to Pay is not a product of a single company, but is based on the Secure Remote Commerce (SRC) standard developed by EMVCo (the joint standards body of the major card networks).

The interesting backstory is that Mastercard (Masterpass) and Visa (Visa Checkout) previously went their separate ways. However, they recognized that the fragmented market – where cards had to be saved differently at every merchant – was hindering progress and giving room to tech giants like Apple and Google. The “competitive situation” was thus replaced by cooperation: a common industry standard was created that funnels every card type under a single recognizable icon, offering a card-network-controlled alternative to Google Pay and Apple Pay.

For consumers, Click to Pay eliminates the need to physically enter card details.

One-time registration: The buyer registers their card for the first time through their bank’s mobile app or a Click to Pay-enabled webshop checkout page. They provide their email address and phone number.

Recognition: When the buyer visits a webshop that supports the technology, the system automatically recognizes them based on their email address or browser cookies.

Selection: Previously saved cards are displayed (only the last 4 digits and card image are visible). No need to type card numbers, expiry dates, or security codes (CVV/CVC).

Authentication and payment: For higher security levels, the system sends a one-time password (OTP) via SMS or email, or the transaction needs to be approved in the banking app (biometric authentication).

● Convenience: Works on any device (laptop, tablet, mobile), regardless of browser.

● Security: The merchant never sees the actual card data, only receives a token.

● Always up-to-date: If the physical card expires and the bank issues a new one, this can automatically update in the background in the Click to Pay profile (network tokenization), so re-registration is not necessary.

For merchants, Click to Pay is a technological “connector” that increases sales and reduces risks.

Integration: The merchant activates the Click to Pay button on the checkout page through their payment service provider (PSP – e.g., SimplePay, Barion).

Token request: When the buyer clicks to pay, the merchant’s system does not request card details. Instead, the system sends a query to the card network (Mastercard/Visa).

Receiving a Digital Token: The card network sends back a unique, encrypted digital token and a one-time cryptogram to the merchant.

Initiating the transaction: The merchant forwards this token to the bank for settlement. Since the token is only valid for that specific merchant and transaction, hackers cannot do anything with it in the event of a data breach.

● Higher conversion: Fewer abandoned carts, as payment is faster and simpler.

● Lower Fraud: Tokenized transactions are more secure, resulting in fewer disputed transactions (chargebacks).

● SCA compliance: The system has built-in handling of Strong Customer Authentication (SCA) requirements, so the merchant doesn’t have to deal with this separately.

The technology was first introduced in the United States at the end of 2019, followed by global expansion from 2020 (Australia, Brazil, United Kingdom, etc.).

The numbers speak for themselves:

● Conversion: Measurements show that payment conversion for new buyers using Click to Pay reaches 96%, while for returning buyers it is 90%.

● Speed: Compared to manual card entry, payment time is on average 20–40% shorter.

● Security: Thanks to tokenization (where a digital identifier travels instead of actual card data), the risk of fraud is significantly lower.

Mastercard’s goal is that by 2030, manual card data payments will be completely phased out in Europe, with every transaction being tokenized (Click to Pay or other digital wallet-based).

Hungarian Situation:

In Hungary, the service is already available to cardholders of most major banks, as Mastercard and Visa have integrated a significant portion of domestic portfolios at the system level.

● OTP Bank: One of the most active supporters, where card tokenization is encouraged through the mobile banking app or Simple account.

● MBH Bank: Dedicated campaigns and customer information materials support Click to Pay registration for Visa and Mastercard cards.

● Erste Bank: Provides full support for both debit and credit cards.

● K&H Bank: Smooth registration is provided for Mastercard cardholders.

● Fintech providers: Revolut and Curve cards (which have a significant Hungarian user base) are compatible with the global Click to Pay system by default.

Most Hungarian webshops do not directly develop the Click to Pay button themselves, but receive it as an update through their payment gateway.

● SimplePay (OTP Mobile): As the largest domestic provider, it continuously activates the Click to Pay option for its merchants. You can find it at partners such as Libri, Bookline, or eMAG’s Hungarian site (where SimplePay provides the backend).

● Barion: In the domestically developed Barion Smart Gateway system, alongside saved card payments, the unified Click to Pay direction has already appeared in thousands of smaller and medium-sized Hungarian webshops (e.g., clothing stores, electronics retailers).

● Borgun / Teya: An internationally backed but extremely popular provider in Hungary, which has made SRC (Secure Remote Commerce)-based payments available in the tourism and services sector (e.g., accommodation booking sites, food delivery).

● Global merchants with a domestic presence: At giants such as Pizza Hut, Emirates, or Wizz Air, Hungarian buyers can regularly encounter the “tilted pentagon” icon at the end of the payment process.

The biggest obstacle to adoption is not technical, but psychological.

Educational gap: Many buyers are still afraid to “save” their card to a cloud, even though Click to Pay is actually more secure than entering physical card data.

Merchant integration: Although major providers already offer it, updating custom-developed payment pages at smaller webshops is time-consuming.

Prerequisites: Bank card issuer support and the buyer’s one-time registration are required (during which the card is linked to their email address and phone number).

Card networks and banks use various tools to support adoption:

● Convenience factor: The device recognition feature (if we mark our device as trusted, not even a code is needed) is the strongest attraction.

● Educational campaigns: Continuous content creation and video tutorials help users with registration.

● Promotions: Periodically, discounts are available at certain merchants when choosing the Click to Pay option.

● Security education: Card networks (mainly Visa) are currently running digital catch-up programs for SMEs that emphasize the advantages of tokenization against fraud.

● Registration convenience: Most banks no longer require separate manual data entry; the card can be “sent” to the Click to Pay wallet with a single button press in the mobile banking app.

Summary: Click to Pay is a new, card-network-supported alternative payment method that enables convenient payment with a single click without entering card details. It is far from as widespread and in many cases not as convenient as payment providers’ own saved card solutions, or as Google Pay or Apple Pay, but in the coming years it could be one of the fastest-growing services.

From a merchant’s perspective, its introduction is not yet critically important today, but it will become interesting for an increasingly large group of buyers. It is likely that in the coming months and years, every payment service provider who wants to remain competitive in the long term will introduce it.

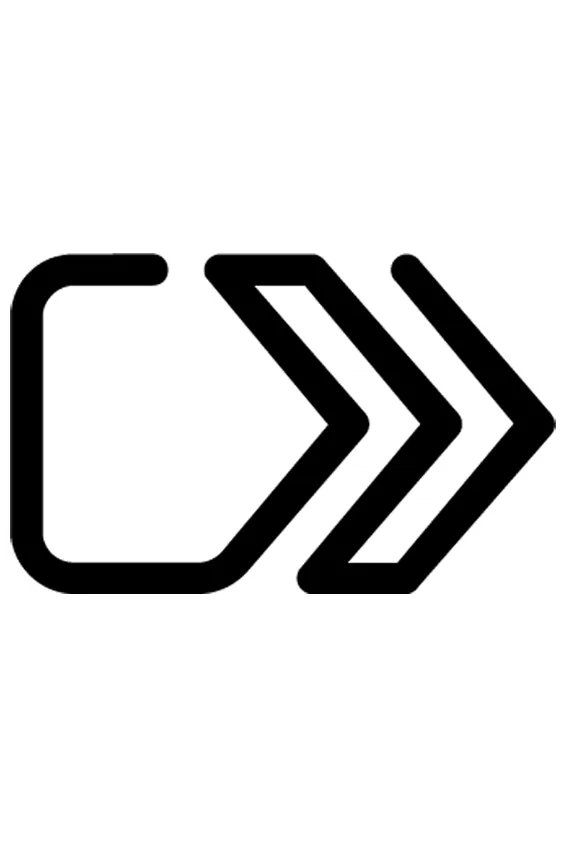

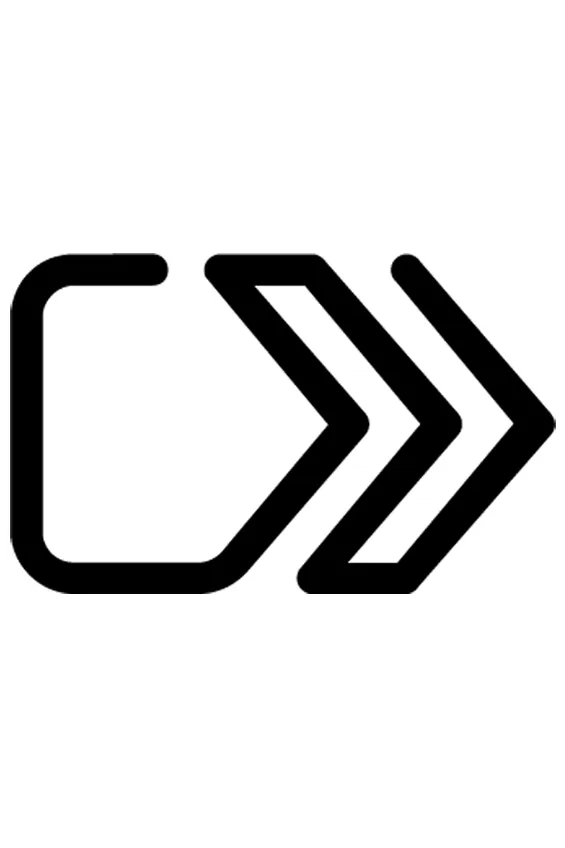

In webshops, you don’t necessarily have to look for the “Mastercard” or “Visa” label, but rather the unified EMVCo Click to Pay icon: a tilted pentagon with a double right-pointing arrow inside it (fast forward symbol).

This video visually demonstrates how Click to Pay works and the recognizability of the icon, which is crucial for the user education mentioned in the article:

Weekly summary of the best POS terminal offers

We handle your data confidentially. Details in the privacy policy.